In its recently published study „European Rail Freight Transport Market“, SCI Verkehr analyses the situation of European rail freight as well as its medium-term perspectives. Unsatisfactory financial performance, high volatility and instability as well as the growing demands of customers in combination with strong competition from modern and environmentally friendly trucks put further pressure on the companies.

Despite a moderate recovery in transport performance in the past two years, the rail freight sector cannot compete with the growth of road transport – it is losing market shares. While the competition on the road is compliant with Euro 6 standards and aiming at other innovations such as self-driven electric trucks, the majority of rail freight companies are hesitant with regard to optimizing its processes and introducing new technologies for boosting its productivity. SCI Verkehr recommends the establishment of a consistent examination of logistical process chains along which appropriate digital instruments and standards for the improvement of profitability.

The transport performance of railways has recovered slightly thanks to an economic pick-up: Most countries with the exception of Belgium as well as the Baltic and Scandinavian states showed moderate growth rates. The market volume of rail freight transport grew by 3% compared to 2012 to a current EUR 17.5 billion, while the modal share of railway decreased further. The successes of Switzerland and Austria have remained isolated cases compared to the rest of Europe.

SCI Verkehr expects a growth in the rail freight sector of around 1% p.a. to 2019. However, high volatility is to be expected: The current signs point at a difficult year 2016.

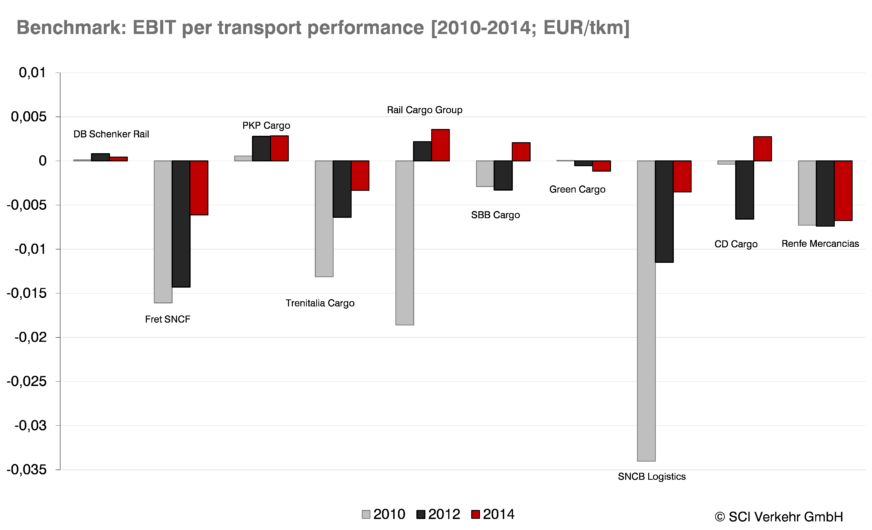

The economic results of many companies remain unsatisfactory. The majority of railway companies have recognized the necessity for restructuring and consolidation and partly taken initial action. However, especially public shareholders oftentimes lack the willingness to implement crucial reform steps und make necessary investments.

In the course of consolidation processes, various mergers and company acquisitions have already taken place while further ones are in the offing. There is increasing interest in railway assets from logistics providers, shipping companies and private equity companies: The Portuguese operator CP Carga was acquired by MSC Rail, parts of LT and Crossrail were acquired by Rhenus-Group and private equity companies have gotten involved with SNCB Logistics, Hector Rail, Freightliner and CTL Logistics.

The new MultiClient Study European Rail Freight Transport Market is available as from now in English language from SCI Verkehr GmbH.